CHINA YUCHAI INTERNATIONAL (CYD)·H2 2025 Earnings Summary

China Yuchai Crushes Estimates as Data Center Demand Surges 167%

February 24, 2026 · by Fintool AI Agent

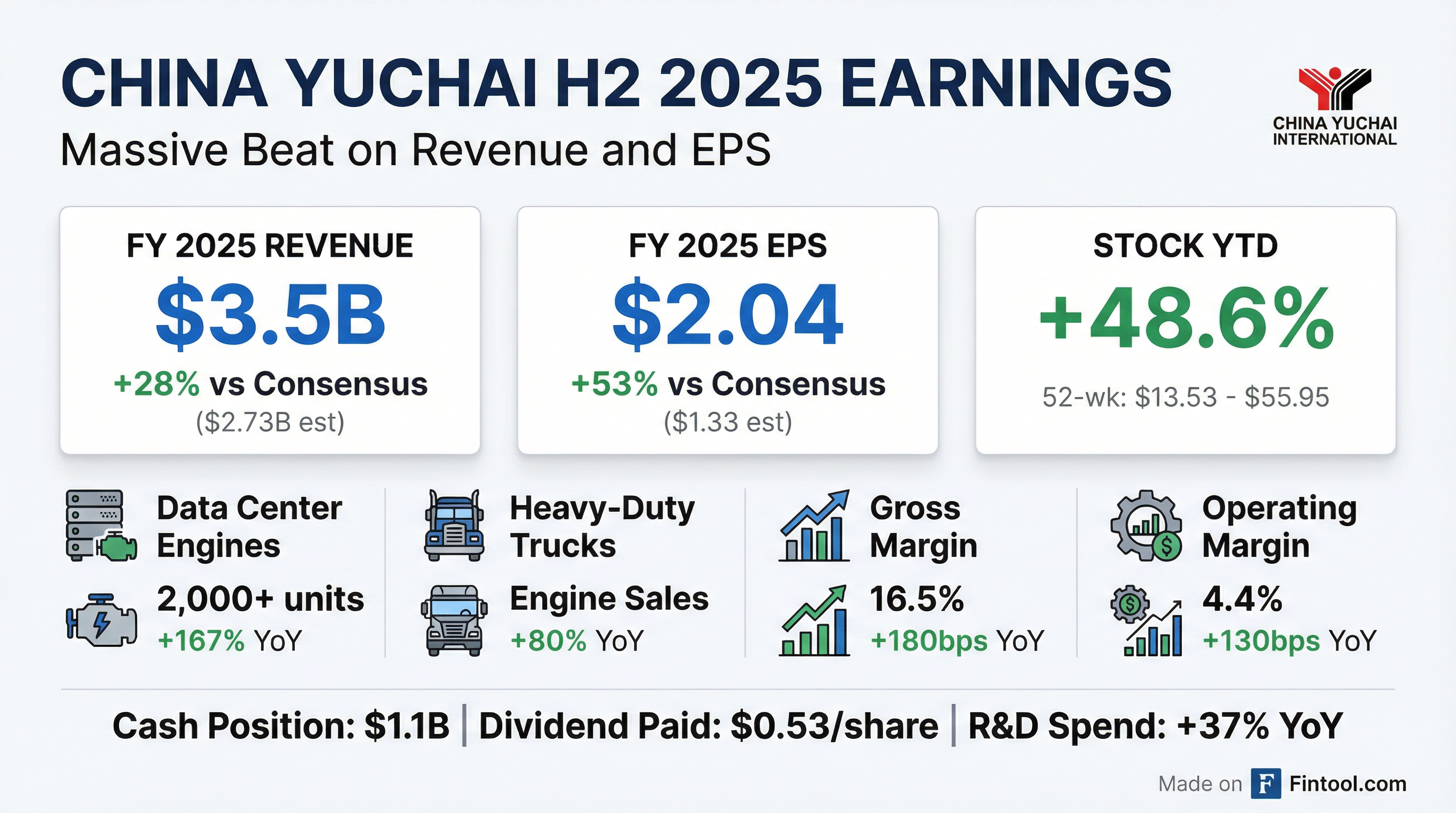

China Yuchai International (NYSE: CYD) delivered a blowout fiscal 2025, with revenue of $3.5 billion crushing consensus estimates by 28% and EPS of $2.04 beating by 53%. The Chinese diesel engine manufacturer's stock has rallied 138% over the past year, driven by explosive demand for data center backup power generators and a resurgence in heavy-duty truck sales.

Did China Yuchai Beat Earnings?

Decisively yes. CYD posted one of the largest beats in its recent history:

Values retrieved from S&P Global

The full-year results reflected strong execution across both vehicle and off-road segments:

For the full fiscal year:

What Drove the Beat?

Data Center Demand Explodes

The standout growth driver was data center backup power generators, where Yuchai's high-horsepower engine sales surged 167% YoY:

"Combined sales of MTU Yuchai Power and Yuchai branded high-horsepower engines to data centers exceeded 2,000 units in 2025, up from 750 units in the prior year."

The MTU Yuchai joint venture generated RMB 211 million in profit, up 22% YoY, though profit growth lagged volume gains due to product mix shift away from higher-margin 20-cylinder engines.

Heavy-Duty Trucks Roar Back

Truck engine sales dramatically outperformed the broader Chinese market:

Management attributed the outperformance to:

- Government "Qianwangsi" replacement policy driving fleet upgrades

- New OEM partnerships with major vehicle manufacturers reaching fruition

- National VI emissions compliance driving replacement demand

How Did the Stock React?

CYD closed at $55.03 on February 23, 2026, near its 52-week high of $55.95. The stock has been on a remarkable run:

The aftermarket trade showed shares at $49.00, suggesting some profit-taking despite the strong results. With expectations now elevated, investors may be questioning sustainability of the data center and truck growth rates.

What Did Management Guide?

Management provided qualitative commentary rather than specific numbers:

Data Centers: "We expect that to improve by double digits this year for the data centers."

Trucks: "We do expect to see a continued growth in that area" for heavy-duty truck engines, driven by expanded OEM relationships.

Overall: Non-data center sales expected "more or less the same if the government continues with the policies from last year."

Risks to guidance:

- Government incentive policies remain uncertain for 2026

- Government grants fell to half of 2024 levels and may remain depressed

- Supply chain constraints for joint venture (MTU) components from Germany

What Changed From Last Quarter?

Margin Expansion Accelerated

Gross margin reached 18.9% in H2 2025 vs. 15.9% in H2 2024, driven by:

- Higher volumes leveraging fixed costs

- Favorable mix shift toward heavy-duty and high-horsepower engines

- Continuing cost reduction initiatives

R&D Investment Ramped Up

R&D expenses surged 37.3% to RMB 1.4B ($192M), representing 6.2% of revenue, focused on:

- National VII emissions standard preparation (expected in 2-3 years)

- Alternative fuel engines: hydrogen, methanol, and ammonia combustion

- Range extender EV systems for commercialization

- Fuel cell development (though impairments were taken)

Strategic Investments

- Nanye Tiankong acquisition — 27.97% stake in fuel injection systems specialist, securing supply chain for common rail systems

- Guangxi Yuchai Double Growth Fund — LP position in PE fund for emerging technology investments

- Hong Kong IPO filing — Marine and genset power subsidiary filed for HK listing in January 2026

Capital Allocation and Balance Sheet

Yuchai maintains a fortress balance sheet with significant optionality:

Shareholder Returns: Paid $0.53 per share dividend in July 2025, demonstrating commitment to capital returns.

Key Q&A Highlights

On tax rate spike (44% in H2): CFO noted non-cash deferred tax asset write-offs of ~RMB 100M distorted the rate. Normalized effective tax rate is 20-21%.

On natural gas engines for data centers: Yuchai has 2MW natural gas generator technology ready, but Asian customers currently prefer diesel economics.

On export opportunities: Yuchai-brand exports remain ~10% of volume, focused on Asia. Joint venture exports account for 20-25%, also primarily Asian markets.

On order backlog for data centers: Delivery lead times remain 3-4 months. Management continues "working very hard to fulfill requirements."

Forward Catalysts

- National VII emissions standards — Expected in 2-3 years, could drive another replacement cycle

- Hong Kong IPO — Marine/genset subsidiary listing would provide growth capital and valuation transparency

- OEM expansion — New vehicle manufacturer partnerships reaching commercialization

- Data center build-out — AI infrastructure demand supporting high-horsepower generator sales

Risks and Concerns

- Government policy dependency — Truck sales heavily reliant on replacement incentive policies

- Reduced government grants — Other operating income down 22.5% YoY as grants tightened

- Supply chain constraints — German component supply limiting MTU joint venture capacity

- Agricultural weakness — Off-road agricultural engine sales declined, offsetting marine/industrial gains

- Valuation — Stock up 138% in one year; expectations now elevated

The Bottom Line

China Yuchai delivered exceptional results that significantly exceeded expectations, driven by structural demand for data center backup power and cyclical recovery in heavy-duty trucks. The 28% revenue beat and 53% EPS beat reflect both market share gains and margin expansion from favorable mix.

Looking ahead, the data center opportunity appears durable as AI infrastructure buildout accelerates, while truck momentum depends on government policy continuity. The balance sheet remains rock-solid with $1.1B cash, providing optionality for M&A, R&D, and shareholder returns.

After a 138% rally, the stock faces elevated expectations — the aftermarket drop suggests some investors are taking profits. The key question for 2026: can Yuchai maintain growth momentum as comparisons toughen and policy support potentially fades?

Related Links: